By Jihoon Lee

SEOUL (Reuters) - South Korea's government will put its focus on supporting people's livelihoods and managing risk factors, as it cut the country's 2024 GDP forecast and raised its inflation projection.

In its biannual economic policy plan released on Thursday, the finance ministry expected the economy to grow 2.2% in 2024, down from 2.4% seen in July, after expanding 1.4% in 2023 which was a three-year low.

The ministry expected consumer prices to rise 2.6% this year, up from its previous forecast of 2.3%. In 2023, prices rose 3.6%.

"The economic recovery will be stronger (than last year) amid improvements in global trade and demand for semiconductors, but there will be difficulties in domestic demand and people's livelihoods due to persistently high inflation and interest rates," the ministry said.

The government will primarily focus on economic recovery for the common people, while managing potential risk factors, it said.

South Korea's exports rose for a third straight month in December as demand for chips started to pick up, raising hopes for an economic recovery driven by semiconductor exports.

The country's central bank has maintained its policy interest rate at 3.5%, the highest since late 2008, since the last hike in January 2023, in its continued fight against slowly easing, but still high inflation.

The finance ministry said it aims to bring down inflation, which stood at 3.2% in December, to the 2% level within the first half of 2024, with more policy measures, such as tax and tariff cuts, and freezing public utility costs.

To boost consumption, the government plans to raise tax exemptions on credit card spending and continue efforts to attract more foreign tourists, including the exemption of visa issuance fees for group tourists from China and other Asian countries.

For companies, the ministry said it will introduce new temporary tax cuts on investments in research and development and extend existing tax breaks on facility investments until end-2024.

The ministry said it will expand liquidity support measures if needed to prevent a credit crunch in builders and real estate projects. Last month, a mid-sized builder applied for a debt restructuring, raising concerns over the construction sector.

BEIJING (Reuters) - China's services activity expanded at the fastest pace in five months thanks to a solid rise in new business, a private-sector survey showed on Thursday, lifting the degree of optimism in the sector to a three-month high.

The data, offering a snapshot of business sentiment, was in contrast to an official survey on Sunday which showed a sub-index of services activity shrank again at the end of 2023, raising calls for more stimulus measures in the new year.

The Caixin/S&P Global services purchasing managers' index (PMI) rose to 52.9 in December from November's 51.5, above the 50-mark separating growth from contraction and posting the highest reading since July.

Aided by robust new business which expanded at the fastest rate since May, firms attributed the improvement to rising customer numbers and spending.

"The overall number of customers rose slightly in December compared with November," said a restaurant owner surnamed Jin, based in Hangzhou, a city in eastern Zhejiang province.

"But still, businesses in 2023 were worse than 2022 due to the macro economic trend," Jin said.

Foreign demand for Chinese services also increased last month. Around 214,000 travellers from France, Germany, Italy, the Netherlands, Spain, and Malaysia entered China in December after the visa-free policy took effect, up 28.5% from November, according to the National Immigration Administration.

Improved demand conditions led firms to increase their staffing levels as they planned to meet rising business requirements. A sub-index of employment returned to expansion in December following November's contraction.

Services firms remained upbeat about their business activity in 2024, with the level of positive sentiment increasing to a three-month high, though it was still below the series average.

Taken together with the better-than-expected Caixin manufacturing PMI, the Caixin/S&P's composite PMI rose to 52.6 last month from November's 51.6, the highest reading since May.

The vibrancy in the services sector extended to the new year as travel data suggest an improvement in the number of domestic visitors during the three-day New Year's holiday from Saturday to Monday.

However, the downbeat PMI survey by the National Bureau of Statistics (NBS) suggests the world's second-largest economy is still under pressure as the once-mighty property sector fails to show any meaningful rebound, consumers are tightening their belts and factories have been cutting selling prices.

Analysts interpret the divergence between Caixin PMI and the official PMI as differences in their geographic and sector coverage.

To spur growth, China's central bank made 350 billion yuan ($49.01 billion) in loans to policy banks through its pledged supplementary lending (PSL) facility in December, increasing market bets that China would cut interest rates further.

The NBS will release economic indicators including industrial output and retail sales in coming weeks.

($1 = 7.1417 Chinese yuan renminbi)

By Noel Randewich

(Reuters) - U.S. chip stocks added to a string of losses on Wednesday, with Wall Street's main semiconductor benchmark tumbling from record highs following its strongest year since 2009, when the sector bounced back after the financial crisis.

Drops of over 2% in Advanced Micro Devices (NASDAQ:AMD), Qualcomm (NASDAQ:QCOM) and Broadcom (NASDAQ:AVGO) weighed most on the PHLX semiconductor index, which was down 2.1%.

The chip index has now declined almost 7% since reaching a record high close on Dec. 27.

This week's drop in semiconductor stocks has tracked a broad Wall Street decline as investors await the Federal Reserve's December meeting minutes due later on Wednesday for clues on its interest rate path.

Fueled by optimism about artificial intelligence and more recently by expectations the Fed will cut interest rates this year, the PHLX surged 65% in 2023, its strongest performance since 2009. That compares to annual gains of 43% and 24%, respectively, for the Nasdaq and S&P 500.

Chip stocks have also benefited from bets that a downturn in global demand last year that saw memory chip makers cut production has largely bottomed out.

Nvidia (NASDAQ:NVDA), viewed as the top provider of AI-related chips, saw its stock market value more than triple in 2023 to $1.2 trillion, making it Wall Street's fifth most valuable company. It dipped almost 1% on Wednesday.

In a client note, BofA Global Research analyst Vivek Arya recommended exposure to cloud computing and cars through stocks including Nvidia, Marvell (NASDAQ:MRVL) Technology, NXP Semiconductors (NASDAQ:NXPI) and ON Semiconductor (NASDAQ:ON). Arya also recommended stocks including KLA Corp and Arm Holdings (NASDAQ:ARM) for exposure to the increasing complexity of chip designs.

In another note, Wells Fargo analyst Joe Quatrochi said he expects a muted recovery for chip equipment sellers in 2024, and pointed to KLA and Applied Materials (NASDAQ:AMAT) as top picks in that industry.

By Marcela Ayres

BRASILIA (Reuters) - Brazil's record 2023 trade surplus may be tough to repeat this year, private economists and government officials agree, as falling interest rates are expected to boost imports.

Brazil's oil, mining and farm sectors have built a robust trade surplus over the past decade that is the envy of many regional peers.

However, last year's surplus grew more than 50% from 2022 to nearly $100 billion largely due to a 12% drop in imports, as the value of exports was almost flat.

That dynamic is likely to change this year, analysts say, as fixed investments are seen rebounding from a 2023 slump due to falling interest rates and major public infrastructure projects drawing private partners.

Data over the past decade show Brazil's fixed investments and imports typically move in tandem. In the third quarter, fixed business investment recorded its fourth straight quarterly drop, a sequence last seen in early 2016, when Brazil grappled with one of its worst recessions in history.

Slumping 2023 imports, along with stronger volumes of farm and mineral exports that offset weaker prices, lifted Brazil's trade surplus to a record. That helped cut the current account deficit in 12 months through October to 1.62% of GDP, the lowest since February 2018.

"It seems important...and little-discussed that the improvement in the trade balance and current account is also a reflection of the low dynamism of investments," said Gilberto Borça Jr., an associate researcher at FGV Ibre.

Even if investments do not surge dramatically, they are likely to rebound in 2024, he added, which could also lift imports.

A government trade official, who requested anonymity to discuss internal forecasts, said the government does not consider the level of the 2023 trade surplus to be structural.

Exports are being supported by higher volumes, which may be hard to maintain, said the official, while stronger investments are likely to boost imports.

After a year of high borrowing costs, Brazilian industry expects a more favorable environment in 2024 due to lower interest rates, said Igor Rocha, chief economist at the Sao Paulo State Industries Federation (Fiesp).

After keeping interest rates at a six-year high to curb inflation, Brazil's central bank kicked off an easing cycle in August and has already cut its policy rate by 200 basis points to 11.75%, signaling further reductions ahead.

LONDON (Reuters) - British business leaders have turned more pessimistic about the outlook for the country's economy and they are holding back on investment decisions, according to a survey published on Wednesday.

The Institute of Directors' (IoD) confidence index - which maps the gap between business leaders who are optimistic about the economy and those who are pessimistic - fell to -28 in December from -21 in November, having gradually risen since June.

Expectations for business investment, costs and wages, and headcount were all little changed.

Despite the caution, company leaders were more upbeat about prospects for their own businesses with hopes for revenue and export growth rising.

Roger Barker, policy director at the IoD, said sentiment among directors had been largely stuck in the doldrums over the second half of 2023 as the impact of higher interest rates took its toll on the economy.

"Although aspects of the business environment have improved in the last couple of months, particularly with regard to inflation, this is not yet exerting a meaningful impact on business decision-making," Barker said.

The IoD called on the Bank of England to start cutting interest rates in early 2024.

"With inflationary pressures abating, business is in dire need of a boost if it is to help drive meaningful economic growth in 2024," Barker said.

The BoE raised Bank Rate 14 times in a row between December 2021 and August last year, since when it has held its benchmark rate at a 15-year high of 5.25%. Governor Andrew Bailey and other top officials have signalled they want to keep borrowing costs high to ensure inflation pressures are snuffed out.

The IoD survey was based on 703 responses from companies polled between Dec. 14 and Dec. 29.

By Caroline Valetkevitch

NEW YORK (Reuters) - U.S. corporate earnings should improve at a stronger clip in 2024 as inflation and interest rates come down, analysts predict, but worries about slowing economic growth hang over the outlook.

S&P 500 earnings are expected to increase 11.1% overall in 2024 after rising a modest 3.1% last year, according to estimates compiled by LSEG.

But earnings growth needs to be enough to support lofty valuations in stocks. The S&P 500 index is trading at 19.8 times forward 12-month earnings estimates, well above its long-term average of 15.6 times, based on LSEG Datastream data.

Falling rates helped drive a sharp year-end rally, especially after the Federal Reserve in December opened the door to interest rate cuts in 2024 after a rate hike campaign that started in 2022.

The Dow Jones industrial average in December hit its first record high close since January 2022, while the S&P 500 is within striking distance of its all-time closing finish. The S&P 500 rose 24.2% for the year.

"The market trading where it is at current levels demands earnings to show strong growth next year," said Sameer Samana, senior global market strategist at Wells Fargo Investment Institute.

Among concerns for 2024 is the lingering effect of higher interest rates on the economy and corporate earnings, he said.

The U.S. government confirmed in December that economic growth accelerated in the third quarter. Gross domestic product increased at a 4.9% annualized rate last quarter, the Commerce Department's Bureau of Economic Analysis (BEA) said in its final estimate.

Profit estimates could weaken further as companies begin to open their books on the fourth quarter and give guidance for the first quarter and the rest of 2024. The release of fourth-quarter results will kick into high gear in mid-January.

"We're definitely seeing those (first quarter) estimates weakening at a faster pace," said Nick Raich, chief executive of The Earnings Scout. "Look at a name like FedEx (NYSE:FDX), and that's a good bellwether of the global economy."

FedEx shares tumbled 12.1% Dec. 20, a day after the package delivery company reported earnings for the quarter ended Nov. 30 that fell short of analysts' targets and cut its full-year revenue forecast.

Estimated year-over-year earnings growth for S&P 500 companies for the first quarter of 2024 is now at 7.4%, down from 9.6% on Oct. 1, based on LSEG data. For the fourth quarter of 2023, S&P 500 earnings are forecast to rise 5.2%, down from 11% growth seen on Oct. 1.

To be sure, investors point to cooling inflation as a strong positive for companies in 2024.

"The consumer still seems to be healthy, inflation is getting better, employment is still strong, interest rates are going down and gas at the pump is going down," said Gary Bradshaw, portfolio manager at Hodges Capital Management in Dallas.

Moreover, "these companies have streamlined their businesses and margins are decent," he said.

U.S. prices fell in November for the first time in more than 3-1/2 years, pushing the annual increase in inflation further below 3%, a recent Commerce Department report showed.

Optimism over growth in artificial intelligence is likely to continue to help companies with results and outlooks tied to AI technology.

"While the rebound in TECH+ (earnings per share) began in 2Q23, earnings for the rest of the market are expected to follow in the year ahead," Jonathan Golub, chief U.S. equity strategist & head of portfolio analytics at UBS Investment Research, wrote in December.

The "Magnificent 7" group of megacap stocks - Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOGL), Amazon.com (NASDAQ:AMZN), Nvidia (NASDAQ:NVDA), Meta Platforms (NASDAQ:META), and Tesla (NASDAQ:TSLA) - accounted for 62.18% of the S&P 500's total return in 2023, according to S&P Dow Jones Indices senior index analyst Howard Silverblatt.

Also, the Fed's recent dovish pivot has boosted the case for the U.S. dollar to weaken, which would make U.S. exporters' products more competitive abroad.

But whether 2024 earnings forecasts are assuming too many of these positives remains a concern.

"The market is assuming a near-perfect landing with inflation cooling without a significant impact to demand and pricing power — not likely in our view," J.P. Morgan equity strategists wrote in their 2024 outlook.

"Current consensus S&P 500 forward EPS growth at 30%ile (+11%)... is in harmony with a Goldilocks outlook for growth and inflation.

By David Lawder

WASHINGTON (Reuters) - International Monetary Fund Managing Director Kristalina Georgieva said Americans should "cheer up" about the U.S. economy, as inflation subsides further in 2024 amid a strong job market and moderating interest rates.

Georgieva told CNN in an interview that aired on Tuesday that the U.S. economy is "definitely" headed for a "soft landing" with fairly strong growth prospects.

"People should be feeling good about the economy because they finally would see relief in terms of prices," Georgieva said, praising the Federal Reserve's "decisiveness" in raising interest rates to fight inflation.

"While that has been painful, especially for small businesses, it has brought the desired impact without pushing the economy into recession," Georgieva added.

Asked why many polls show Americans pessimistic about the economy, the IMF chief said that consumers had become accustomed to low inflation and very low interest rates for many years, and when both jumped in recent years, it was a shock.

"My message to everyone is, you have a job and interest rates are going to moderate this year because inflation is going down. Cheer up. It is a new year, people," Georgieva said.

Georgieva repeated her warnings against fragmentation of the global economy along geopolitical lines due to increasing national security restrictions, with countries gravitating towards separate blocs led by the United States and China.

Allowed to continue, she said this could ultimately reduce Global GDP by 7% - roughly equal to the annual out put of France and Germany," and urged Washington and Beijing to compete on a rational basis, while cooperate on globally important issues.

"So we are all better off to find ways to reduce frictions, to concentrate on security concerns that are real and meaningful, and not go willy-nilly in fragmenting the world economy. We would end up with a smaller pie," Georgieva said.

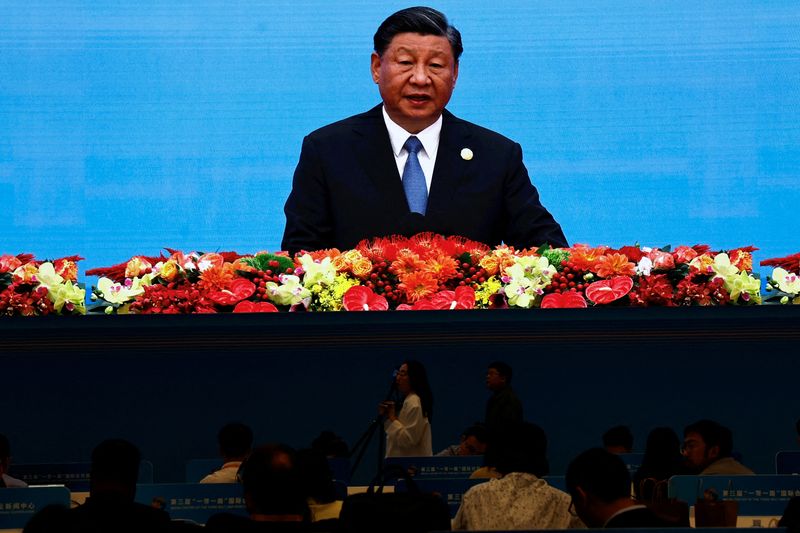

BEIJING (Reuters) - President Xi Jinping said on Sunday that China will consolidate and enhance the positive trend of its economic recovery in 2024, and sustain long-term economic development with deeper reforms.

In a televised speech to mark the New Year, Xi said China would deepen reforms to shore up confidence in the economy.

Xi said China will "consolidate and enhance the positive trend of economic recovery, and achieve stable and long-term economic development," Xi said.

"We must comprehensively deepen reform and opening up, further boost confidence in development, enhance economic vitality, and make greater efforts to promote education, promote science and technology, and cultivate talents."

Xi voiced his concerns over difficulties facing some firms' operations and the hardship facing some people in employment and their daily lives, and the impact of natural disasters such as floods and earthquakes in some regions.

China will promote high-quality development and balance development and security in a well-coordinated way, Xi added.

The government has in recent months announced a series of measures to shore up China's feeble post-pandemic economic recovery, which is being held back by a property slump, local government debt risks and slow global growth.

Analysts expect China's economic growth to hit the official target of around 5% this year, and Beijing is expected to maintain the same target next year.

Earlier this month, top Chinese leaders met and laid out economic plans for 2024, pledging to take more steps to support the recovery. The central bank has pledged to step up policy adjustments to support the economy and promote a rebound in prices, amid signs of rising deflationary pressures.

By Ankur Banerjee

SINGAPORE (Reuters) -The dollar rose on the first trading day of the year as attention turned to economic data this week that may provide clues on the Federal Reserve's next moves, while bitcoin surged above $45,000 for the first time since April 2022.

The dollar index, which measures the U.S. currency against six rivals, fell 2% in 2023, snapping two years of gains. It was last at 101.54, up 0.158%, as investors weighed the prospect of the Fed cutting rates this year.

The dollar's ascent weighed on the Japanese yen the most, with the Asian currency down 0.54% at 141.63 per dollar, having slid 7% in 2023.

Rescue teams in Japan on Tuesday struggled to reach isolated areas hit by a powerful earthquake on New Year's Day, with reports of more than 20 people dead in a disaster that toppled buildings and knocked out power to thousands of homes.

Markets are now pricing in an 86% chance of interest rate cuts from the Fed to start from March, according to CME FedWatch tool, with over 150 basis points (bps) of easing anticipated in the year.

"The question is when and how fast rate cuts will be delivered," Marc Chandler, chief market strategist at Bannockburn Global Forex, said in a note.

"Moderating price pressures and weaker growth impulses have seen the pendulum of market sentiment swing dramatically from the 'higher for longer' mantra of most of last year to pricing in aggressive easing" from central banks, Chandler said.

The focus now switches to a slew of economic data due this week, including the data on job openings and nonfarm payrolls. Minutes from the last Fed meeting in December are scheduled for release on Thursday and will provide insight into the central bankers' thinking around rate cuts this year.

"The positive sentiment from end-2023 may roll over into this week as all eyes turn to the U.S. jobs report on Friday," said Nicholas Chia, macro strategist at Standard Chartered (OTC:SCBFF).

At its December policy meeting, the Fed adopted an unexpectedly dovish tone and forecast 75 basis points in rate reductions for 2024.

That contrasted with other major central banks, including the European Central Bank (ECB) and Bank of England (BoE), which reiterated they will hold rates higher for longer.

Still, traders are pricing in 158 bps of cuts by the ECB this year, while the BoE is also expected to cut rates by 144 bps in 2024.

The euro was down 0.2% at $1.1022, inching away from the five-month peak of $1.11395 it touched last week. The single currency gained 3% last year, its first yearly gain since 2020.

Sterling was last at $1.27105, down 0.15% on the day, having clocked its strongest yearly performance last year since 2017 with a 5% gain.

Elsewhere, the Australian dollar was little changed at $0.68105. The New Zealand dollar was 0.3% lower at $0.6300.

The crypto world started the year with a bang, with bitcoin touching a 21-month peak of $45,511, up 3% on the day on rising expectations that the U.S. Securities and Exchange Commission would soon approve exchange-traded spot bitcoin funds.

========================================================

Currency bid prices at 0353 GMT

Description RIC Last U.S. Close Pct Change YTD Pct High Bid Low Bid

Previous Change

Session

Euro/Dollar $1.1024 $1.1046 -0.20% -0.13% +1.1046 +1.1019

Dollar/Yen 141.5350 141.0450 +0.38% +0.38% +141.6600 +140.9400

Euro/Yen 156.04 155.66 +0.24% +0.26% +156.1600 +155.4500

Dollar/Swiss 0.8443 0.8416 +0.34% +0.34% +0.8448 +0.8409

Sterling/Dollar 1.2714 1.2730 -0.11% -0.08% +1.2735 +1.2710

Dollar/Canadian 1.3255 1.3245 +0.08% -0.01% +1.3256 +1.3224

Aussie/Dollar 0.6814 0.6810 +0.07% -0.04% +0.6822 +0.6803

NZ 0.6300 0.6319 -0.30% -0.30% +0.6323 +0.6295

Dollar/Dollar

All spots

Tokyo spots

Europe spots

Volatilities

Tokyo Forex market info from BOJ

한국어

한국어

Tiếng Việt

Tiếng Việt

中文

中文