WASHINGTON (Reuters) - The U.S. will provide up to $250 million in arms and equipment to Ukraine in the final package of aid this year to help Kyiv in its war with Russia, Secretary of State Antony Blinken said on Wednesday.

President Joe Biden has asked Congress to provide another $61 billion in aid to Ukraine, but Republicans are refusing to approve the assistance without an agreement with Democrats to tighten security along the U.S.-Mexico border.

The White House has warned that without the additional appropriation U.S. aid will run out by the end of the year for Ukraine's fight to retake territory occupied by Russian forces since it invaded in February 2022.

Blinken said the latest aid package included air defense munitions, additional ammunition for high-mobility artillery rocket systems, artillery ammunition, anti-armor munitions and over 15 million rounds of ammunition.

Congress has approved more than $110 billion for Ukraine since Russia's invasion, but it has not approved any funds since Republicans took control of the House of Representatives from Democrats in January 2023.

By Koh Gui Qing and Dhara Ranasinghe

NEW YORK/LONDON (Reuters) -World stocks rallied to their highest level in more than a year on Wednesday, while the U.S. dollar hit a five-month low, as expectations mounted that key central banks such as the Federal Reserve will start to cut interest rates early next year.

In line with expectations of lower interest rates, the benchmark 10-year Treasury yield fell to a five-month low, while the two-year Treasury yield tumbled to a low not seen in seven months.

Investor hopes that monetary conditions might be loosening boosted the MSCI's gauge of stocks across the globe by 0.46% to a level not seen since October 2022.

On Wall Street, the Dow Jones Industrial Average added 0.21%, while the S&P 500 and the Nasdaq Composite were flat.

European shares edged up 0.21%, with trade subdued given public holidays across the region on Monday and Tuesday.

Analysts said the main risk for markets was that rates might not fall as fast as expected.

"If global equity markets have one Achilles' heel going into January 2024, it is the expectation that the Fed will be methodically and consistently cutting interest rates throughout the year," said Nicholas Colas, Co-founder of DataTrek Research.

The benchmark 10-year Treasury yield fell to 3.793%, and the 2-year yield retreated to 4.2375%. [US/]

Expectations of rate cuts also dragged on the U.S. dollar, which fell 0.51% against a basket of six major currencies to a level last seen on Jul. 27. [USD/]

The jovial mood in world equity markets and a sluggish dollar lifted the euro by 0.54% to $1.1102, more than a four-month peak.

“If the Fed cuts rates because inflation has come so far down that they don’t want policy to unintentionally tighten ... then that’s probably a good scenario,” said Lou Brien, market strategist at DRW Trading in Chicago.

If they cut because of a weakening economy, however, “then the history is kind of harsh” for the economy and the stock market. “The motivation behind the rate cuts is still unknown and is going to be the most important factor,” Brien said.

Market pricing shows a more than 80% chance the Fed is likely to begin cutting rates next March, according to the CME FedWatch tool, with over 150 basis points of easing priced in for all of 2024.

Oil prices slipped as some major shippers returned to the Red Sea - an area disrupted after Yemen's Houthi militant group began targeting vessels earlier this month.

U.S. crude fell 2.02% to $74.04 per barrel and Brent was at $79.6, down 1.81% on the day.

Maersk shares fell more than 4.5%, and other shipping stocks also declined, giving back part of this month's gains that were driven by expectations a Red Sea traffic halt could boost rates.

In Asia, MSCI's broadest index of Asia-Pacific shares outside Japan rose more than 1% to an over four-month high.

China's November industrial profits posted double-digit gains as overall manufacturing improved, data showed, although soft demand continued to constrain business growth expectations, emboldening calls for more macro policy support.

Japan's Nikkei rallied more than 1%, and Hong Kong's Hang Seng Index rose 1.7% in its first trading day after the Christmas and Boxing Day holidays. Chinese blue chips eked out a marginal gain of 0.35%.

Spot gold added 0.5% to $2,077.39 an ounce [GOL/], while Bitcoin jumped rose 2.08% to $43,393.00.

By Ankur Banerjee

SINGAPORE (Reuters) -The dollar remained under pressure on Wednesday and the euro was close to a four-month peak, as expectations that the Federal Reserve would soon cut interest rates took hold in the market, with thin year-end flows keeping movements limited.

With many traders out for holidays, volumes are likely to be muted until the New Year.

The dollar index, which measures the U.S. currency against six rivals, was at 101.47, just shy of the five-month low of 101.42 it touched last week. The index is on course for a 1.9% drop in 2023 after two straight years of strong gains, driven by first the anticipation of and then the actual hiking of rates by the Fed to battle inflation.

"With little to speak of on the economic calendar for this week between global holidays, we do not expect a large swing in pricing to wrap up this calendar year," analysts at Monex USA said in a note.

The recent weakness in the dollar - the index is set to clock a second straight month of losses - has been the result of the markets anticipating rate cuts from the Fed next year, denting the appeal of the greenback.

Markets are now pricing in a 79% chance of a rate cut starting in March 2024, according to CME FedWatch tool, with over 150 basis points of cuts priced in for next year.

Data showing cooling inflation has emboldened bets of easing next year.

"Disinflation is proving entrenched (and) expectations are for central banks to pivot next year while growth is still trudging along," said Christopher Wong, a currency strategist at OCBC in Singapore.

"This paints a goldilocks market that is favourable for risk proxies."

The Australian dollar and the New Zealand dollar both touched a fresh five-month peak earlier in the session. The Aussie last bought $0.6828, while the kiwi was at $0.6333.

Meanwhile, the euro was down 0.04% at $1.10385, having touched a four-month high of $1.1045 on Tuesday. The single currency is up nearly 3% in the year and is on course for a third straight month of gains, matching the run it had last year.

The Japanese yen weakened 0.14% to 142.58 per dollar and is headed for an 8% drop in the year although the Asian currency has witnessed a bout of strength in recent weeks as traders wager that the Bank of Japan will soon exit its ultra-loose policy.

A summary of opinions at the central bank's Dec. 18-19 meeting showed that BOJ policymakers saw the need to maintain its ultra-easy monetary policy for now, with some calling for a deeper debate on a future exit from massive stimulus.

The summary of opinions was somewhat dovish and showed no sense of urgency to end the ultra-loose policies, according to Saxo strategists.

The likely timing of the end of the policies will be later than what the market is anticipating, the Saxo strategists said in a note.

========================================================

Currency bid prices at 0555 GMT

Description RIC Last U.S. Close Pct Change YTD Pct High Bid Low Bid

Previous Change

Session

Euro/Dollar $1.1041 $1.1043 +0.00% +3.05% +1.1044 +1.1029

Dollar/Yen 142.5600 142.3900 +0.17% +8.69% +142.8400 +142.4500

Euro/Yen 157.41 157.23 +0.11% +12.20% +157.6700 +157.1600

Dollar/Swiss 0.8535 0.8537 -0.01% -7.69% +0.8545 +0.8535

Sterling/Dollar 1.2730 1.2723 +0.03% +5.24% +1.2732 +1.2720

Dollar/Canadian 1.3189 1.3195 -0.06% -2.67% +1.3210 +1.3187

Aussie/Dollar 0.6828 0.6825 +0.05% +0.18% +0.6840 +0.6818

NZ 0.6333 0.6329 +0.09% -0.24% +0.6336 +0.6321

Dollar/Dollar

All spots

Tokyo spots

Europe spots

Volatilities

Tokyo Forex market info from BOJ

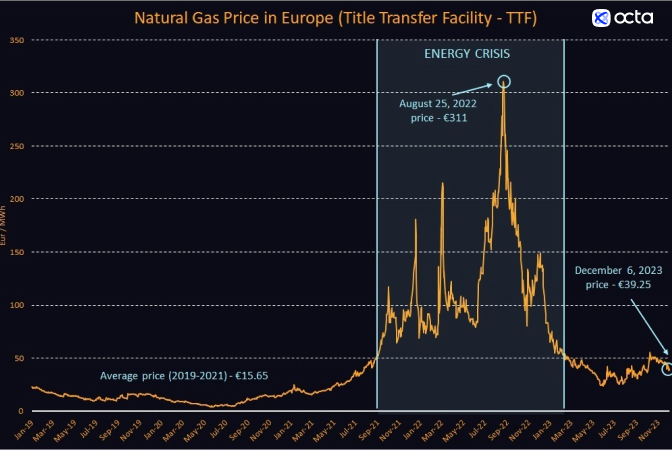

Europe faced an unprecedented energy crisis for around seventeen months (from September 2021 to February 2023), as coal, natural gas, and electricity prices surged to all-time highs. Governments across the continent rushed in to introduce energy-saving measures and implement conservation policies, while households and businesses had to cut consumption rapidly.

Now, as 2023 draws to a close, can we confidently conclude that the energy crisis in Europe is over? How prepared is Europe to cope with the upcoming winter? What are the risks and challenges that lie ahead?

The energy crisis's most acute phase occurred in the summer of 2022. One only needs to look at the evolution of Europe's benchmark natural gas price (TTF) to assess the scale of the emergency (see the chart above). On 25 August 2022, TTF price reached €311 per megawatt-hour (MWh), the highest level ever recorded. On that specific day, the price was 44% above the previous maximum reached on March 7, 2022, and was a staggering 18 times higher than the three-year average price recorded over 2019-2021. Despite Europe's gas storage sites being 78% full in August 2022, supply worries were rife as imports from Russia dropped by around 60%, forcing Europe to rely extensively on liquefied natural gas (LNG) imports—especially from the United States. However, the aggregate supply of LNG in the global market at that time was reduced as one of the U.S. LNG export plants—Freeport LNG—had to go offline due to an explosion incident. Thus, to secure an adequate number of LNG cargoes, Europe had to outbid other customers in South and East Asia by agreeing to pay higher prices to suppliers.

A lot has changed since last summer. The European gas prices have returned to normality but remain above the level observed before the crisis. On Monday, 6 December, the front-month futures contract for delivery in January at TTF settled at €39.25 per MWh, 87% below the peak observed in August 2022 but still some two times above the historical average seen in 2019-2021. Kar Yong Ang, Octa analyst singles out several reasons for normalisation:

‘Although natural gas prices in Europe remain higher than they were before the crisis, the situation has improved dramatically. There are several reasons for this. First, there was a structural loss of demand partly due to reduced economic activity and partly due to conservation policies. Second, imports of pipeline gas and that of LNG increased. On top of it, there was a bit of luck as well, as weather conditions allowed the Europeans to build the stocks faster than normal.’

Indeed, probably the most painful adjustment that Europe had to endure was the loss of demand. According to Eurostat, total gas use in the EU's top 6 consuming countries—Germany, Italy, France, Netherlands, Spain, and Poland—was down by 17% in the first ten months of 2023 compared with the five-year average for 2017-2021. Obviously, energy-intensive industries such as chemicals and steel production had to bear the brunt of adjustment. For example, according to Statistisches Bundesamt, Germany's energy-intensive manufacturing production has decreased by about 20% since the start of 2022 and has not shown any signs of recovery yet.

Thus, Europe had to rely on imports more and more to balance its natural gas market. Russia has long been the main supplier of affordable pipeline gas into Europe, but geopolitical tensions, sanctions, and explosions of the Nord Stream pipeline have brought the flows to a minimum. According to Eurostat, Russia exported just 22.3 billion cubic metres of natural gas into Europe in the first nine months of 2023, which is 57% lower than during the same period in 2022 and 65% lower than during the same period in 2021. Concurrently, imports of LNG from the United States reached 30.01 billion cubic metres during the first nine months of the year, up a whopping 185% from the same period in 2021.

‘Overall, Europe has managed to bring its natural gas inventories to a rather comfortable level and is now well-protected to withstand future supply shocks,’ says Kar Yong Ang, Octa analyst. Indeed, according to the latest data from Gas Infrastructure Europe, gas storage levels are at record highs for this time of the year at around 94% full, said the Octa analyst, adding that the general bias for TTF price remains bearish. ‘I would not be surprised to see European natural gas prices drop to €30 per MWh in case of a normal winter. Alternatively, if this upcoming winter turns out to be colder than normal, we might see TTF temporarily hitting €60 per MWh.’

However, Kar Yong Ang says that different kinds of challenges and risks lie ahead for Europe. ‘It appears that Europe is placing too much faith in LNG. It's betting too much on a single supply source, which may backfire in the long run. If Europe is to permanently replace relatively cheap pipeline imports from Russia with expensive LNG imports, then, I am afraid, economic activity in its traditional industries may never recover to the pre-crisis levels.’

Indeed, Europe's top competitors—the United States and China—benefit from lower prices. The United States has ample resources at home, while China is getting cheap imports from Russia. Europe risks losing its competitive standing in the global marketplace. Furthermore, as we explained at the beginning of the article, the temporary shutdown of a single LNG export plant in the U.S. has already highlighted how strongly European energy security is now connected with the intricacies of the global LNG market. Most recently, Houthi militants in Yemen have stepped up attacks on vessels in the Red Sea, which has already prompted some LNG vessels to reroute in order to avoid Bab-el-Mandeb strait between Yemen and Djibouti. So far, the maritime attacks in the region have had a much stronger impact on the price of oil, but natural gas and LNG markets could also be affected.

‘With supply options more limited than in the past, European consumers will have to get used to more volatile natural gas prices, as they will increasingly be determined by the whims of the weather and by the bargaining power of other LNG importers in Asia,’ says Kar Yong Ang, Octa analyst.

Europe has survived the energy crisis and managed to adapt but has done so at the cost of lower demand and reduced economic activity. Now, Europe will have to learn to navigate the global LNG trade successfully to secure the most favourable deals.

By Hyonhee Shin

SEOUL (Reuters) - North Korean leader Kim Jong Un has kicked off a key meeting of the country's ruling party, state media KCNA reported on Wednesday, setting the stage for unveiling policy decisions for the new year.

The ninth Plenary Meeting of the 8th Central Committee of the Workers' Party of Korea wraps up a year during which the isolated country enshrined nuclear policy in its constitution, successfully launched a spy satellite and fired a new intercontinental ballistic missile (ICBM).

The days-long assembly of the party and government officials has been used in recent years to make key policy announcements. Previously, state media released Kim's speech on New Year's Day.

On the first day of the meeting on Tuesday, participants discussed six major agenda items, including this year's policy and budget implementation, a draft budget for 2024 and ways to bolster the party's leadership, KCNA said.

Kim "defined 2023 as a year of great turn and great change," lauding progress in all areas including the military, economy, science and public health despite some "deviations," it said.

He presented a detailed report involving "indices of the overall national economy which is clearly proving that the comprehensive development of socialist construction is being pushed forward in real earnest," KCNA said.

The development of new strategic weapons including the reconnaissance satellite has put the country "on the position of a military power," it added.

Tension has rekindled in recent weeks after North Korea tested its newest ICBM which it said was aimed at gauging the war readiness of its nuclear forces against mounting U.S. hostility.

Kim also said last week that Pyongyang would not hesitate to launch a nuclear attack if an enemy provokes it with nuclear weapons.

The United States, South Korea and Japan condemned the missile test, and activated a system to detect and assess North Korea's missile launches in real-time and established a multi-year trilateral military exercise plan.

LONDON (Reuters) - Ethiopia became Africa's third default in as many years on Tuesday after it failed to make a $33 million "coupon" payment on its only international government bond.

Africa's second most populous country announced earlier this month that it intended to formally go into default, having been under severe financial strain in the wake of the COVID-19 pandemic and a two-year civil war that ended in November 2022.

It had been supposed to make the payment on Dec. 11, but technically had up until Tuesday to provide the money due to a 14-day 'grace period' clause written into the $1 billion bond.

According to two sources familiar with the situation, bondholders had not been paid the coupon as of the end of Friday Dec. 22, the last international banking working day before the grace period expires.

Ethiopian government officials did not respond to requests for comment on Friday or over the weekend, but the widely-expected default will see it join two other African nations, Zambia and Ghana, in a full-scale "Common Framework" restructuring.

The East African country first requested debt relief under the G20-led initiative in early 2021.

Progress was initially delayed by the civil war but, with its foreign exchange reserves depleted and inflation soaring, Ethiopia's official sector government creditors, including China agreed to a debt service suspension deal in November.

On Dec. 8, the government said parallel negotiations it had been having with pension funds and other private sector creditors that hold its bond had broken down.

Credit ratings agency S&P Global then downgraded the bond, to "Default" on Dec. 15 on the assumption that the coupon payment would not be made.

(Reuters) -U.S. retail sales rose 3.1% between Nov. 1 and Dec. 24, as shoppers looked for last-minute Christmas deals amid big promotions, a Mastercard (NYSE:MA) report showed on Tuesday.

The increase is lower than the 3.7% growth Mastercard forecast in September and last year's 7.6% rise as higher interest rates and inflation pressured consumer spending.

Amazon.com (NASDAQ:AMZN) and Walmart (NYSE:WMT) ramped up promotions through November in the United States to entice bargain-hunting shoppers, but analysts said that the discounts were not as deep as the prior year, when retailers were saddled with excess stock after the pandemic.

Some of those discounts were rolled back starting in December, when customers were expected to buy last-minute gifts and household goods on the Saturday before Christmas - dubbed "Super Saturday."

Arun Sundaram, an analyst at CRFA Research, said many shoppers waited for Black Friday and Cyber Monday to make holiday purchases and finished the final sprint during Super Saturday.

"Consumers are still spending, but they're still price conscious and want to stretch their budgets," Sundaram said. He said the weeks between Cyber Monday and Super Saturday were a "soft period" for spending, but shoppers used the final weekend before Christmas to look for "big deals."

Ecommerce sales grew at the slower pace of 6.3% compared to last year's 10.6% as the popularity of online shopping came off pandemic highs, the report showed.

Sales in the apparel and restaurant categories rose 2.4% and 7.8%, respectively, during the holiday shopping period, according to the Mastercard SpendingPulse report, while sales of electronics fell 0.4%.

Mastercard SpendingPulse measures in-store and online retail sales across all forms of payment. It excludes automotive sales.

LONDON (Reuters) - Ethiopia became Africa's third default in as many years on Tuesday after it failed to make a $33 million "coupon" payment on its only international government bond.

Africa's second most populous country announced earlier this month that it intended to formally go into default, having been under severe financial strain in the wake of the COVID-19 pandemic and a two-year civil war that ended in November 2022.

It had been supposed to make the payment on Dec. 11, but technically had up until Tuesday to provide the money due to a 14-day 'grace period' clause written into the $1 billion bond.

According to two sources familiar with the situation, bondholders had not been paid the coupon as of the end of Friday Dec. 22, the last international banking working day before the grace period expires.

Ethiopian government officials did not respond to requests for comment on Friday or over the weekend, but the widely-expected default will see it join two other African nations, Zambia and Ghana, in a full-scale "Common Framework" restructuring.

The East African country first requested debt relief under the G20-led initiative in early 2021.

Progress was initially delayed by the civil war but, with its foreign exchange reserves depleted and inflation soaring, Ethiopia's official sector government creditors, including China agreed to a debt service suspension deal in November.

On Dec. 8, the government said parallel negotiations it had been having with pension funds and other private sector creditors that hold its bond had broken down.

Credit ratings agency S&P Global then downgraded the bond, to "Default" on Dec. 15 on the assumption that the coupon payment would not be made.

MANILA (Reuters) - Philippine President Ferdinand Marcos Jr. has approved the extension of reduced tariffs on rice and other food items until the end-2024 to keep prices stable amid a threat of dry weather in the coming months, his office said on Tuesday.

The modified rates first approved in 2021 had already been extended this year due to high inflation, and Marcos said another extension was needed until the end of next year.

"The present economic condition warrants the continued application of the reduced tariff rates on rice, corn, and (pork)...to maintain affordable prices for the purpose of ensuring food security," Marcos was quoted as saying in a statement.

Inflation was at 4.1% in November, easing for a second straight month, but has averaged 6.2% in the first 11 months of 2023, well outside the Philippine central bank's 2%-4% target for the year.

The extension of the modified tariffs, Marcos said, is aimed at ensuring affordable prices of rice, corn and meat products with the looming effects of the El Nino dry weather phenomenon early next year and the continued threat of African Swine Fever.

The tariff rate for rice will remain at 35%, while import levies on corn will stay at 5%-15% and 15%-25% for pork products, according to the new executive order extending the modified tariff rates.

NEW DELHI (Reuters) - The Indian government said on Friday a warning from the International Monetary Fund (IMF) that the country's debt to GDP ratio could hit 100% was a worst-case scenario, and not a "fait accompli".

The IMF, in a so-called article IV review, said India's general government debt, which includes federal and state government debt, could be 100% of GDP under adverse circumstances by fiscal 2028.

India's finance ministry said this was "a worst-case scenario and is not fait accompli".

India's debt to GDP ratio, which was 81% in 2022/23, may decline to below 70% in the same period under favourable circumstances, the IMF report also said, according to the ministry.

"Therefore, any interpretation that the report implies that General Government debt would exceed 100% of GDP in the medium term is misconstrued," the ministry added.

한국어

한국어

Tiếng Việt

Tiếng Việt

中文

中文